Weekly Checkup

August 9, 2024

The Part D Redesign: A Tragedy in Three Acts

Act I: The Promise Restored

The Medicare Prescription Drug, Improvement, and Modernization Act of 2003 contained an audacious promise: to create a new entitlement providing a financial product that did not exist in nature, financial insurance against the cost of outpatient prescription drugs for seniors. It was built on – not in defiance of – the power of private markets to deliver the benefits at low cost. Prescription drug plans (PDPs) would have incentives to negotiate low drug prices, offer low premiums, and harness the purchasing power of millions of seniors.

With Medicare Part D’s launch in 2006, the promise was made real, and it became a successful fixture of the entitlement landscape, offering each senior dozens of plan choices and receiving perennial high marks. Over time, however, the crafty Congress could not resist meddling, tossing in some taxpayer money here, cash from a Pharma raid there, and generally trying to turn this entitlement unicorn into a run-of-the-mill, tax-and-spend federal program.

As the calendar turned to 2022, Congress passed the Inflation Reduction Act (IRA). The otherwise-desultory IRA contained a valuable redesign of the basic Part D benefit, built upon years of work at AAF and elsewhere. The basic idea was a return to the Part D roots: strong incentives to control costs by making PDPs liable for a greater share of the costs – especially catastrophic costs – tying pharmaceutical firms’ contributions to the price of drugs and keeping individuals from reaching the catastrophic limit. Beneficiaries and taxpayers would be much better protected against the costs of outpatient drugs.

The sun shone brightly. A light, humidity-free breeze wafted through the nation’s capital, children sang, and the country was united by a vision of the Steelers as Super Bowl champions.

Act II: The Promise Dashed

And then – surprise! – the election approached. Congress and the Biden Administration had somehow forgotten that 2024 was an election year. Together, they made no provision to phase in or otherwise manage the return of strong cost-saving pressures. The increased responsibility to cover the cost of the benefit inevitably forced the plans to stay in business by scrambling to raise premiums.

As John Walker noted in his insight on the situation, premiums rose by 21 percent from 2023 to 2024. With the arrival of full premium pressures, Walker asks, “how much might Part D premiums jump in response to a 179-percent increase in bid amount compared to last year?”

Under the threat of electoral backlash, the Centers for Medicare and Medicaid Services announced a “Premium Stabilization Demonstration,” which would funnel $7.2 billion to insurers, reducing the need to raise premiums and keeping the plans in business. Just like that, the market incentives disappeared, and Part D was pushed back to being a borrow-and-spend entitlement program.

And in the streets, the children screamed, the lovers cried, and the poets dreamed. But not a word was spoken – the promise had been broken.

Act III: Groundhog Day

The near-term threat has seemingly been neutralized, but the real evil is the three-year nature of the “Stabilization Demonstration.” It removes any incentive for the plans to change their business models to accommodate the new pressures on premiums and costs.

What, then, will happen as the “Demonstration” gets close to expiring? Will the threat of higher premiums terrify politicians? Yes. Will the inability to raise premiums threaten the survival of plans? Yes. And will whoever is president and whatever is the Congress provide the money again? Yes.

And three years after that?

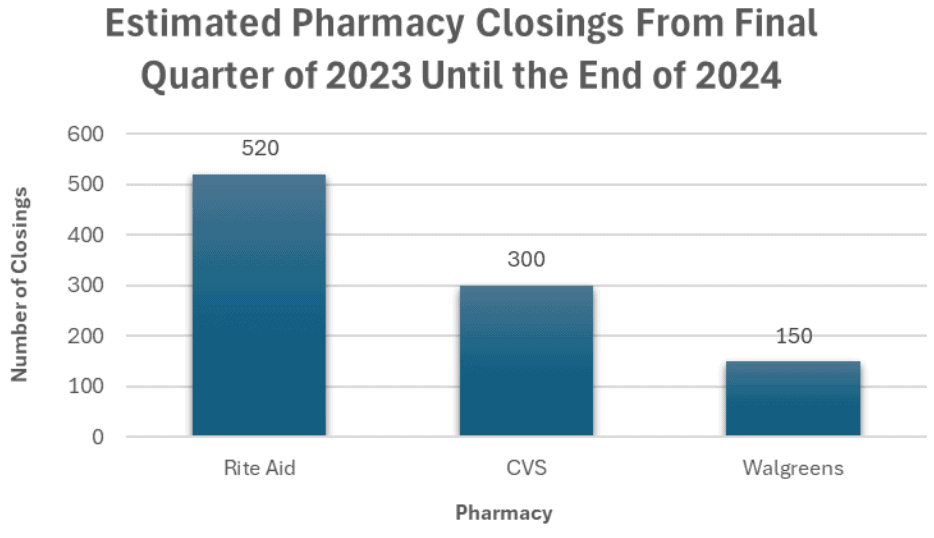

Chart Review: “Pharmacy Deserts” Increase Amid Cost Concerns

Parth Dahima, Health Care Data Analyst

Mass closings of the three largest U.S. pharmacy chains – Walgreens, CVS, and Rite Aid – may affect thousands of consumers. Over the next five years, thousands of stores from the largest chains are expected to close due to mounting competition, staff shortages, and lack of revenue. Independent community pharmacies also face profitability struggles, with gross profit margins falling to the lowest point in 10 years.

The chart below estimates the number of store closures by the largest three brands from the final quarter of 2023 until the end of 2024. Specific estimates beyond August 2024 are unavailable for Walgreens. CEO Tim Wentworth announced potential closures of 25 percent of Walgreens stores due to underperformance, however. CVS has also announced rough estimates, with 300 closings this year and 600 estimated closings in the next four. Rite Aid leads with list with nearly double the number of closings as CVS, fueled mostly by a bankruptcy filing in October 2023.

Sources:

https://ncpa.org/newsroom/news-releases/2023/10/15/ncpa-releases-2023-digest-report

https://www.cnbc.com/2024/06/27/walgreens-wba-earnings-q3-2024.html

https://restructuring.ra.kroll.com/RiteAid/

https://www.cbsnews.com/news/rite-aid-closing-stores-pharmacies

https://www.nbcchicago.com/news/local/walgreens-announces-plans-to-close-150-stores-in-us/3173352/