Testimony

May 22, 2024

Testimony on: “Burdensome Regulations: Examining the Biden Administration’s Failure to Consider Small Businesses”

United States House of Representatives Committee on Small Business

* The views expressed here are my own and not those of the American Action Forum.

Chairman Williams, Ranking Member Velázquez, and members of the Committee, thank you for convening this hearing and providing the opportunity to discuss the economic impacts small businesses face from recent rulemakings and ways federal agencies can improve how they examine and adjust these rulemakings to provide some degree of targeted regulatory relief.

In my testimony I wish to make three main points:

- The regulatory record for federal agencies currently stands at an unprecedented level under the Biden Administration with total estimated costs from final rulemakings exceeding $1.6 trillion since the current administration came into office;

- While, of course, not all these costs fall directly on small businesses, there has been a subset of rules that will have an outsized impact on small businesses, whether they carry an official Regulatory Flexibility Act (RFA) designation or not; and

- An examination of this overall increased volume of significant rulemaking reveals potential deficiencies in the current RFA analytic framework worth remedying, including the need for greater consideration of the cumulative impact of multiple rulemakings, further analysis of indirect costs imposed on small businesses by rules for which the RFA currently does not apply, and more robust agency acknowledgement of small business concerns overall.

Let me consider these in turn.

The Overall Biden Administration Regulatory Record

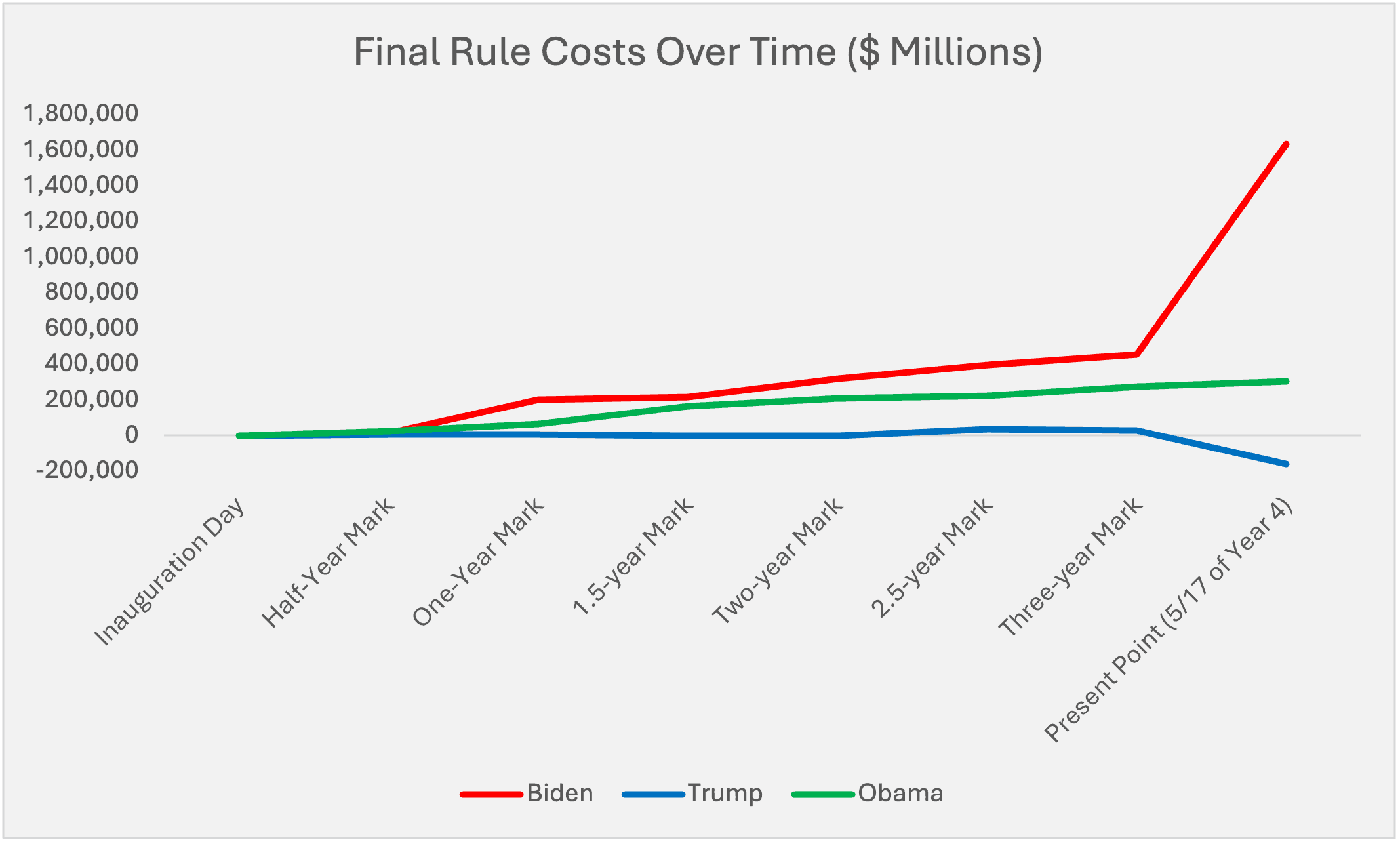

The level of regulatory activity under the Biden Administration has been immense. As of May 17, the total estimated costs from final rules emanating from federal agencies under the current administration added up to more than $1.6 trillion. For perspective, this sum exceeds the federal government’s current projected fiscal year (FY) 2024 budget deficit by more than $100 billion and is roughly equivalent to the gross domestic product of Spain.

This estimate is not one I came up with through some stand-alone projection or model, but rather by simply cataloguing the agencies’ own quantified estimates in their rulemaking analyses. This total represents the agencies’ own calculations. The scale of this figure is even more jarring when compared to the two immediately preceding administrations. The Biden Administration’s current final cost total is more than five times that of the total accumulated by agencies through this point in the Obama Administration.

![]()

What’s more is that a sizeable portion of these costs was finalized in only the past few weeks. As the graph below illustrates, the Biden Administration has consistently been ahead of its predecessors throughout this term. As of early April, its regulatory cost total had already surpassed the total imposed under the entire first term of the Obama Administration. Then, largely due to a single rule (the Environmental Protection Agency’s (EPA) latest “tailpipe rule” for passenger vehicles) that total jumped well past the entirety of the Obama Administration and into trillion-dollar territory. Ensuing weeks have seen dozens of notable rulemakings that continue to push the total upward and upward at a prodigious pace. In short, since the beginning of this year, the Biden regulatory cost total has essentially quadrupled.

Notable Recent Rulemakings and the RFA

Considering how approximately half of the current Biden regulatory cost comes from the latest EPA tailpipe rule – a rule that does not directly regulate small businesses – it is clear that not all of these costs necessarily fall on small businesses. Nevertheless, as I am sure most of the members of this committee already appreciate, regulatory burdens are generally more acute for small businesses since they inherently have fewer resources at hand to deal with compliance costs compared to the phalanxes of lawyers and other regulatory affairs personnel that large companies can deploy. As such, the Regulatory Flexibility Act (RFA) – one of the main points of our discussion here today – was enacted in order to have agencies address the unique issues small businesses face during the rulemaking process.

Using the RFA analyses included in these agency rulemakings, one can begin to discern which pieces of this $1.6 trillion pie directly apply to small businesses. In examining the 100 costliest rules under the Biden Administration thus far – which account for 99 percent of that overall cost total – I have found 36 rules that contain at least partial acknowledgement of small business impacts. The total combined costs of these rules add up to approximately $235 billion. In 23 of these rules, the agencies have either stated affirmatively and explicitly that the rule “may” or “will” impose a “significant impact on a substantial number of small entities” (sometimes referred to by the acronym: SISNOSE) or implicitly signaled such a determination with the inclusion a full small business impact analysis as required under the RFA. The remaining 13 rules either include a partial RFA analysis or an analysis that finds that while the rule may impact small businesses, such effects do not meet the SISNOSE threshold.

Of those rules that have a clear SISNOSE designation, the most consequential action is the Financial Crimes Enforcement Network (FinCEN) rule regarding “Beneficial Ownership Information Reporting Requirements.” The rule requires “certain entities to file with FinCEN reports that identify two categories of individuals: the beneficial owners of the entity, and individuals who have filed an application with specified governmental authorities to create the entity or register it to do business.” Per FinCEN’s own analysis, this rule’s total costs over a 10-year period could add up to $84.1 billion (using a 7 percent discount rate). In the RFA analysis section, FinCEN states that “that for purposes of estimating costs to small businesses, all reporting companies are small businesses.” Thus, this rule is an example of a regulation where small businesses bear the entirety of the burdens.

The most significant rule from those where the impacts either do not meet the SISNOSE threshold or where such a designation is ambiguous is the recent rule from the Centers for Medicare and Medicaid (CMS) regarding “Minimum Staffing Standards for Long-Term Care [LTC] Facilities and Medicaid Institutional Payment Transparency Reporting.” This rule would require that covered LTC facilities have “an RN [registered nurse] to be on site 24 hours per day and 7 days per week,” and maintain a minimum of “3.48 total nurse staffing hours per resident day (HPRD) of nursing care, with 0.55 RN HPRD and 2.45 NA [nurse aide] HPRD.” CMS estimates that costs involved with meeting these requirements will be more than $43.1 billion over a 10-year period. In the RFA analysis section, CMS finds that annual costs will across the industry amount to 2.2–2.3 percent of total revenue. While the agency admits that “95 percent of the health care entities impacted are considered small businesses,” since the cost-to-revenue ratio is slightly below the “3 to 5 percent” threshold that the agency uses for such determinations, CMS declares that “this final rule will not have a significant economic impact on a substantial number of small entities.”

Areas Where the RFA Could Improve

These examples and others help to illustrate some of the current deficiencies of the RFA process. The LTC staffing rule provides a prime opportunity to review the issue of how agencies establish their threshold for what constitutes “a significant economic impact” while also opening up greater consideration of cumulative regulatory impacts. For instance, another major SISNOSE rule under the Biden Administration was a Food and Drug Administration (FDA) rule regarding “Requirements for Additional Traceability Records for Certain Foods.” In that rule’s RFA analysis, FDA utilizes a 1 percent cost-to-revenue threshold. Granted, per the “Flexibility” part of the RFA’s title, different industries may face different profit margin considerations and require different thresholds, but this is an instance where perhaps it is worth a more rigorous reexamination of why each agency has arrived at its particular RFA threshold.

Additionally, especially in instances where such determinations fall within tenths of a percentage point, there may be value in having agencies take greater consideration of the cumulative regulatory environment. For instance, this recent LTC staffing rule may not result in a given facility incurring costs equal to 3 percent of its revenue by itself, but what if such a facility must also prepare and file the aforementioned Beneficial Ownership reports to FinCEN? What if the recent Department of Labor rule on overtime pay already has this hypothetical facility making significant payroll adjustments on top of those that would be required in hiring the requisite nursing staff? Any of these rules may be well-intentioned and defensible as a stand-alone measure in a vacuum, but in real-world practice they begin to add up quickly – especially if such new regulatory requirements all become operable within a relatively short timeframe.

Another aspect of the economic impact from rulemakings that is also underexplored – if meaningfully explored at all – in RFA analysis is the question of “indirect costs.” A potential example of this is the EPA tailpipe rule discussed earlier. Since the rule’s primary focus is on automobile manufacturers – some of the largest companies in the world – it typically would not be a major part of the RFA discussion. With an overall cost total of $870 billion, however, it is difficult to imagine that it will not have some appreciable downstream effects on small businesses. Take, for instance, this section of the rule’s Regulatory Impact Analysis where EPA estimates the potential per-vehicle cost increases for “medium-duty” vehicles:

EPA notes that these figures do not necessarily represent direct price increases and that certain tax credits may ease the effective burden, but it is reasonable to assume that at least some of these costs will be passed on to the consumer in the form of higher prices. Say you are a small courier business with a fleet of delivery vans or a small construction company with a fleet of work trucks looking to determine when and how to upgrade such fleets in coming years. Having the sticker price of each vehicle potentially be thousands of dollars more than it would be otherwise represents a not-insignificant consideration. While including further indirect cost analysis may not necessarily change the substantive course of a rule like the tailpipe rule, having a more robust understanding of these impacts may help to better inform such exercises as the cumulative impact analysis discussed above.

And finally, beyond instituting new aspects of small business impact analysis, agencies need to be more rigorous and thorough in the RFA analysis they are already supposed to conduct. Roughly one year ago, the Small Business Administration Office of Advocacy (Advocacy) released its Report on the Regulatory Flexibility Act, FY 2022. This annual report details agency responsiveness to Advocacy’s input into the rulemaking process – particularly in its formulation of RFA analyses and of alternatives that could provide regulatory relief for small businesses. In my analysis of this report at the time, I found that the adjustments agencies made to their rules in response to Advocacy’s concerns amounted to merely $73.5 million in cost savings for small businesses, which represented the lowest such figure in a decade. This was despite the fact that: A) FY 2022 had an overall higher level of regulatory activity and B) Advocacy provided more input to agencies than in any of the preceding nine years. Taken together, these factors suggest that agencies do not take the RFA process as seriously as they should.

The RFA has been around for more than 40 years across administrations and Congresses of both parties, serving as an important tool in helping to better craft federal rules by accounting for the inherent asymmetry small businesses face in complying with regulatory requirements versus large businesses. These are not exercises in wanton elimination of federal regulation. Changes made to rules as a part of RFA deliberations are often at the margins and provide targeted relief to the subset of affected entities that need it most. Now, in this current period of unprecedented regulatory activity overall, it is even more important that agencies refocus and expand their efforts in addressing these concerns.

Thank you. I look forward to your questions.