Research

May 31, 2017

The Job Implications of a $15 Minimum Wage in Illinois

Summary Points

- Increasing the minimum wage to $15 per hour in Illinois could cost the state 382,200 jobs by 2025, virtually erasing all job growth over the next decade.

- Illinois is in no position to absorb this shock, as its struggling labor market already lags the rest of the United States.

- The proposed tax credit for businesses with fewer than 50 workers will likely do little to mitigate these negative consequences because most minimum wage employees work for businesses with more than 50 workers and the tax benefit itself is small and temporary.

Introduction

Currently, lawmakers in Illinois are considering a bill that would raise the state’s minimum wage from $8.25 per hour to $15 per hour by 2022. With Governor Bruce Rauner unlikely to support the measure, the minimum wage will certainly become a major policy issue in Illinois this year.[1] While this may be a well-intended effort to improve the livelihoods of low-wage workers, American Action Forum (AAF) research has shown that proposals to raise the minimum wage put low-skilled workers at risk of losing their jobs and fail to deliver substantial raises to low-income households. Illinois is no different, as this massive minimum wage hike would cost the state 382,200 jobs.

Background

Illinois’s minimum wage has been $8.25 per hour since 2011. Under the bill making its way through the Illinois legislature, the state’s minimum wage would increase to $9 in 2018 and gradually rise to $15 in 2022.[2] To help small businesses afford the wage increase, the bill would also establish a tax credit for businesses with fewer than 50 workers. In particular, a business would be able to reduce its state income tax payments by 75 cents for each hour that a minimum wage employee works. Under the proposal, however, the total value of the tax credit would be capped at 25 percent of state tax payments in 2018 and would phase out as the new minimum wage phases in. Specifically, the maximum tax benefit would decline by 5 percentage points each year, and when the minimum wage reaches $15 per hour in 2022, small businesses would be only be able to reduce their state income tax payments by a maximum of 5 percent. The tax credit would then expire at the beginning of 2023.[3]

Labor Market Consequences

While proposals to raise the minimum wage are well intended, it is important to take into account the negative labor market consequences. Meer & West (2015) conclude that raising the minimum wage reduces job creation.[4] Specifically, they find that a 10 percent increase in the real minimum wage is associated with a 0.3 to 0.5 percentage-point decrease in the net job growth rate. As a result, three years later employment becomes 0.7 percent lower than it would have been absent the minimum wage increase.

This may not seem very problematic, but the bill under consideration in Illinois would mandate an 81.8 percent increase in the minimum wage. This means that if the minimum wage were to be $15 by 2022, by 2025 employment would be 5.7 percent lower than under current law. Using the Illinois Department of Employment Security (IDES) employment projections as a baseline,[5] this comes out to a loss 382,200 jobs.[6] To put this figure in perspective, IDES projects that between 2014 and 2024, Illinois is on track to create 371,593 jobs. This means that the 382,200 jobs lost in Illinois due to the proposed $15 minimum wage bill would wipe out all employment growth over the entire decade.

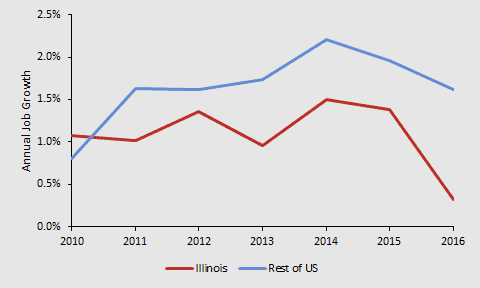

Moreover, Illinois is in absolutely no position to be able to absorb such a large shock to its labor market, which is already struggling. As illustrated in Chart 1, throughout America’s slow economic recovery, job growth in Illinois has lagged behind the rest of the country since 2011.

Chart 1: Annual Job Growth in Illinois and the Rest of the United States, 2010-2016[7]

In 2016, employment in Illinois only grew by 0.3 percent, while jobs in the rest of the country increased by 1.6 percent.

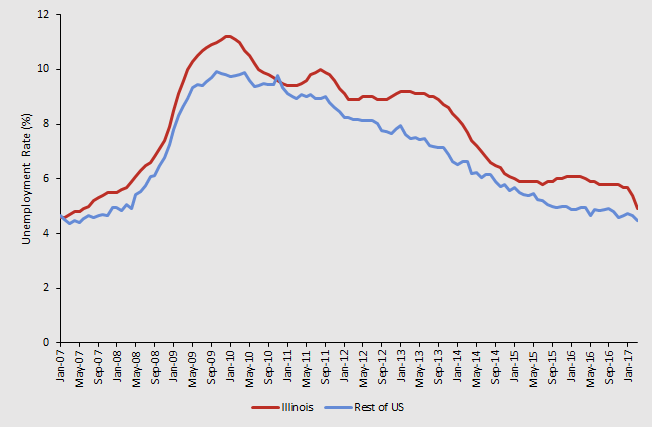

Chart 2 reveals that Illinois was hit particularly hard by the Great Recession, as its unemployment rate rose and remained above the national rate for a decade.

Chart 2: Unemployment Rate in Illinois and the Rest of the United States, 2007-2017[8]

In December 2009, just after the United States’ economic recovery began, the unemployment rate in Illinois peaked at 11.2 percent, while unemployment in the rest of the country was 9.8 percent. Going forward throughout the economic recovery, the unemployment rate in Illinois remained elevated above the rest of the country.

Why the Proposed Tax Credits are Unlikely to Mitigate these Consequences

To help smaller businesses afford the minimum wage increase, the proposed legislation would make a new tax credit available to businesses with fewer than 50 workers. This measure, however, would be unlikely to save many jobs because the 81.2 percent mandated wage increase would far outweigh the temporary tax breaks. In particular, there are four main reasons the tax credit would not save many jobs.

First, the tax credit would only be available to businesses with fewer than 50 workers. While small businesses do disproportionately employ minimum wage workers, the majority of minimum wage employees still work for businesses with over 50 employees. Nationally, 40 percent of workers earning the federal minimum wage work for employers with less than 50 workers.[9] The remaining 60 percent are in larger businesses, which would not benefit from the tax credit in Illinois.

Second, while the minimum wage increase to $15 per hour would be permanent, the tax credit would be temporary. In particular, beginning in 2023, the tax credit would expire and all businesses would face the full cost of the minimum wage increase. In effect, the tax credit only helps small businesses adjust to the minimum wage while it phases in, but it would not help them afford the permanent increase in mandated labor hourly labor costs.

Third, even during the phase-in period, the tax breaks would unlikely help small businesses adjust because the maximum tax breaks would be small and they would illogically decline as the magnitude of the annual wage increase would grow. Table 1 contains the proposed minimum wage increase and maximum tax credit schedule.

Table 1: Proposed Illinois Minimum Wage and Tax Credit Schedule

| Minimum Wage & Tax Credit |

2017 |

2018 |

2019 |

2020 |

2021 |

2022 |

2023 |

| Minimum Wage |

$8.25 |

$9.00 |

$10.00 |

$11.25 |

$13.00 |

$15.00 |

$15.00 |

| Year-to-Year Change |

$0.00 |

$0.75 |

$1.00 |

$1.25 |

$1.75 |

$2.00 |

$0.00 |

| Cumulative Wage Increase |

$0.00 |

$0.75 |

$1.75 |

$3.00 |

$4.75 |

$6.75 |

$6.75 |

| Hourly Tax Credit |

$0.00 |

$0.75 |

$0.75 |

$0.75 |

$0.75 |

$0.75 |

$0.00 |

| Year-to-year effective increase in costs per hour |

$0.00 |

$0.00 |

$1.00 |

$1.25 |

$1.75 |

$2.00 |

$0.75 |

| Cumulative effective increase in costs per hour |

$0.00 |

$0.00 |

$1.00 |

$2.25 |

$4.00 |

$6.00 |

$6.75 |

| Maximum Percent Reduction in Tax Payments |

0% |

25% |

20% |

15% |

10% |

5% |

0% |

The tax credit would provide businesses with $0.75 per hour that a minimum wage employee works. As illustrated in Table 1, 2018 is the only year when this hourly tax credit rate would entirely offset the minimum wage increase, which would rise by $0.75 from $8.25 to $9. However, since the legislation would only allow a business to reduce its state tax payments by a maximum of 25 percent in 2018, the tax credit that year would only partly offset the additional labor costs for most businesses. For instance, suppose a business with fewer than 20 workers earns an annual profit of $200,000, which is typical for a business with fewer than 20 employees in Illinois.[10], [11], [12] Illinois taxes corporate income at a 7.75 percent rate (5.25 percent corporate tax rate plus a replacement tax of 2.5 percent),[13] meaning that the business would pay $15,500 in taxes. Since the tax benefit in 2018 is capped at 25 percent of state tax payments, at most the business’s tax payments would decline by $3,875. So, the credit would only pay for the entire wage increase for 5,200 hours of minimum wage work or 2.5 full-time-equivalent (FTE), year-round minimum wage workers. If the business employs anymore hours of minimum wage work, it would have to bear the additional cost on its own.

Unfortunately, 2018 would be the tax credit’s most generous year. As the new minimum wage phases-in, the magnitude of the wage hike each year would grow. Instead of the maximum tax benefit growing along with the minimum wage, however, the benefit would decline. While the minimum wage would increase by $0.75 in 2018 from $8.25 per hour to $9 per hour, in 2019 it would increase by $1.00 from $9 per hour to $10 per hour. This results in a total wage increase of $1.75 since 2017. In that same year, the maximum tax benefit would decline by 5 percentage points and small businesses would only be able to reduce their state tax payments by 20 percent at most. Looking forward, 2022 would be the largest one-year wage increase, as the minimum wage would rise by $2.00 from $13 per hour to $15 per hour and result in a total wage increase of $6.75 per hour since 2017. In that same year, however, the proposed bill would only allow businesses to reduce state tax payments by 5 percent, only one-fifth of the tax break they would receive for the $0.75 wage increase.

Fourth, even if there were no cap on the tax break and businesses could claim the tax credit for each hour of minimum wage work, the tax credit would not offset the increase in hourly labor costs in any year after 2018. Let’s suppose that under the proposed legislation, there would be no maximum tax benefit available to each small business. As shown in Table 1, in 2018, the $0.75 per hour minimum wage increase would be entirely offset by the $0.75 hourly tax credit. Each year going forward, however, the tax credit would remain flat at $0.75 per hour and only pay for that initial wage hike. As a result, in 2019, businesses would bear the entire $1 wage hike, and $1 of the $1.75 cumulative wage increase since 2017. By 2022, businesses would bear the entire $2 wage hike and $6 of the $6.75 cumulative wage increase. 2022 would be the last year the minimum wage rises. In 2023, however, the $0.75 tax credit would expire, increasing the minimum wage’s cost to businesses by an additional $0.75 per hour and making businesses responsible for the entire cost of the $6.75 minimum wage increase. So, even in a scenario where there is no maximum tax benefit, the tax credit at best would simply defer the cost of the minimum wage increase by only one year. Instead of spending state funds on a costly tax credit, it would make no difference to small businesses if Illinois lawmakers merely delayed the minimum wage increase by a year.

With these shortcomings, it is highly unlikely that the proposed tax credit would save more than a few of the 382,200 jobs that could be lost because in reality no business would rely solely on this tax credit in order to afford the minimum wage increase. Instead, businesses would take measures to cut labor costs or boost profits. To illustrate this point, Table 2 contains the example of an Illinois business with fewer than 20 workers and an annual profit of $200,000 in 2017. In this example, the business employs 3 FTE minimum wage workers and makes no changes to its workforce as the minimum wage rises, relying solely on the tax credit to offset the additional costs. As is clear, without taking steps to cut labor costs or boost profits, the tax credit would not prevent annual after tax profit from substantially declining over time.

Table 2: Small Business Example

| Payroll and Profits |

2017 |

2018 |

2019 |

2020 |

2021 |

2022 |

2023 |

| Minimum Wage |

$8.25 |

$9.00 |

$10.00 |

$11.25 |

$13.00 |

$15.00 |

$15.00 |

| Annual Pay per Minimum Wage FTE |

$17,160 |

$18,720 |

$20,800 |

$23,400 |

$27,040 |

$31,200 |

$31,200 |

| Total Payroll for 3 Minimum Wage FTE |

$51,480 |

$56,160 |

$62,400 |

$70,200 |

$81,120 |

$93,600 |

$93,600 |

| Pre-Tax Profit |

$200,000 |

$195,320 |

$189,080 |

$181,280 |

$170,360 |

$157,880 |

$157,880 |

| Normal Tax Payment |

$15,500 |

$15,137 |

$14,654 |

$14,049 |

$13,203 |

$12,236 |

$12,236 |

| Tax Credit (%) |

0% |

25% |

20% |

15% |

10% |

5% |

0% |

| Tax Credit ($) |

$0 |

-$3,784 |

-$2,931 |

-$2,107 |

-$1,320 |

-$612 |

$0 |

| Tax Payment with Credit |

$15,500 |

$11,353 |

$11,723 |

$11,942 |

$11,883 |

$11,624 |

$12,236 |

| Post-Tax Profit |

$184,500 |

$183,967 |

$177,357 |

$169,338 |

$158,477 |

$146,256 |

$145,644 |

|

Reduction in Post-Tax Profit |

$0 |

-$533 |

-$6,610 |

-$8,019 |

-$10,861 |

-$12,221 |

-$612 |

In this example, in 2017 the business earns $200,000 in profit and pays $15,500 (7.75 percent of its profit) in taxes to the state of Illinois in 2017, before the minimum wage increases. As the new minimum wage phases in, the increase in labor costs would cause both pre-tax and post-tax profit to decline, even after claiming the tax credit.

This would be true even in 2018, when the business would receive the largest tax benefit. In 2018, the minimum wage would increase from $8.25 per hour to $9 per hour. As a result, the total payroll costs for three FTE minimum wage workers would increase from $51,480 to $56,160. If the business were to make no effort to offset the additional labor costs and rely exclusively on the tax credit to pay for the wage hike, the increase in costs would cause pre-tax profit to decline from $200,000 to $195,320. With three FTE minimum wage workers, in each year the business would claim the maximum available tax benefit. In 2018, the tax credit would allow the business to reduce its state tax obligation by 25 percent or $3,784 from $15,137 to $11,353. This would leave the business with a post-tax profit of $183,967, $533 lower than its $184,500 post-tax profit in 2017. So, although the tax credit in 2018 would save the business almost $3,800, the $0.75 minimum wage increase would still leave the business worse off than before, as its post-tax profit would be decline by $500.

To make matters worse, post-tax profit would begin to fall by a much larger degree in each of the following years because the size of the maximum tax benefit would decline as the magnitude of the wage increase escalates. In 2019, after paying for an additional $1 minimum wage increase and only claiming a 20 percent ($2,931) reduction in tax payments, the business’s post-tax profit would decline by another $6,610. Each following year that the minimum wage would phase-in, the reduction in post-tax profit would only grow. In 2022, when the business would be required to pay the entire $15 per hour minimum wage and would only be able to reduce its state tax payments by 5 percent, after-tax profit would $12,221 lower than in 2021.

As shown in Table 3, by the time the tax credit expires in 2023, the business is in much worse condition than in 2017.

Table 3: Loss of Profit and Tax Revenue

| Change in Post-Tax Profit |

2017-2023 |

| Relative to 2017 |

-$38,856 |

| Cumulative since 2017 |

-$125,960 |

| Tax Revenue |

2018-2022 |

| Cumulative Cost of Tax Credit |

-$10,755 |

| Cumulative Revenue Lost due to Reduction in Pre-Tax Profit |

-$11,486 |

| Cumulative Total Loss of Tax Revenue |

-$22,240 |

In 2023, the business’s post-tax profit would be $38,856 (21 percent) lower than it was in 2017. Moreover, cumulatively from 2017 to 2023, the proposed minimum wage bill would cost the business a total of $125,960 in lower post-tax profit. The combination of the reduction in pre-tax profit due to the wage hike and the tax credit would also come at a major cost to the Illinois government. Cumulatively, throughout the minimum wage phase-in period, the tax credit by itself would lead to the business paying $10,755 less in taxes to the Illinois state government. Over the same time period, the reduction in pre-tax profit due to the higher payroll costs would cumulatively lower the business’s state tax payments by an additional $11,486. In total, the proposed minimum wage legislation would reduce the businesses tax payments to the Illinois state government by $22,240 throughout the minimum wage phase-in period.

Clearly, if the business were to not make any changes to reduce its payroll costs or increase profits, the minimum wage bill would lead to substantially less revenue for the Illinois government that already has a budget teetering on disaster.[14] The legislation’s lead sponsor, State Representative Will Guzzardi, has argued that the minimum wage bill pays for itself because if workers earn a higher minimum wage, they will use costly public assistance programs less frequently.[15] While this is a common claim among many minimum wage advocates, there is no statistical evidence that raising the minimum wage lowers government spending.[16] That is because the workers who become jobless when a minimum wage increases are much more likely to utilize government benefits. In addition, workers who earn the minimum wage are not frequently in poverty, as they come from households with a broad range of incomes. For instance, in a previous AAF report we found that only 7 percent of additional earnings from a $15 per hour federal minimum wage would actually go to workers in poverty. 14 percent would go to workers in households with incomes that are six times the poverty threshold.[17]

Of course, in reality a business would not simply rely on the tax credit. Instead, it would act to offset the mandated increase in hourly labor costs to limit any loss of profit. Economics literature has shown that businesses consistently take multiple steps to afford a minimum wage increase. To reduce its labor costs, businesses reduce hiring or eliminate current positions.[18] To increase profits, businesses tend to replace unskilled workers with more productive workers[19] or raise prices.[20] And if a business is still unable to afford the wage hike, as has been the case for several restaurants in San Francisco, it shuts down and leaves its workers without a job.[21] In each case, the most vulnerable workers in the labor force are the ones who bear these costs.

Conclusion

While raising the minimum wage is very popular, it is important for policymakers to understand that it has a major cost. The proposal to raise the minimum wage to $15 per hour in Illinois would be particularly problematic, costing the state 382,200 jobs. With employment only growing 0.3 percent last year, the Illinois labor market is in no position to absorb this shock. Moreover, the tax credit proposed to help small businesses afford the minimum wage increase will not be able to save more than a handful of jobs. This is mainly because it is temporary and its design is flawed, illogically reducing assistance as the magnitude of the minimum wage increase grows. There simply is little reason to think that the tax credit would help businesses or their workers afford an 81.2 percent minimum wage increase.

[1] “Illinois Dems aim high with minimum wage proposal,” Fox 32/AP, April 23, 2017, http://www.fox32chicago.com/news/local/250223060-story

[2] “Amendment to House Bill 198,” Amendment 001, HB 198, March 28, 2017, p. 12, http://ilga.gov/legislation/100/HB/PDF/10000HB0198ham001.pdf

[3] Ibid., pp. 7-10

[4] Jonathan Meer & Jeremy West, “Effects of the Minimum Wage on Employment Dynamics,” Journal of Human Resources, August 2015, http://people.tamu.edu/~jmeer/Meer_West_MinimumWage_JHR-final.pdf

[5] “Long-Term Occupational Projections (2014-2024),” Employment Projections, Illinois Department of Employment Security (IDES), http://www.ides.illinois.gov/LMI/Pages/Employment_Projections.aspx

[6] IDES projects the change in employment growth between 2014 and 2024. To estimate Illinois’ projected employment level in 2025 (three years after the $15 per hour minimum wage is implemented), we calculate the compounded annual total employment growth rate implied by 2014-2024 projection. We then assume the 10-year growth rate remains the same and project total state employment in 2025.

[7] Based on author’s analysis of Bureau of Labor Statistics’ data from Current Employment Statistics, https://www.bls.gov/data/

[8] Author’s analysis of the Bureau of Labor Statistics’ data from Current Population Survey and Local Area Unemployment Statistics, https://www.bls.gov/data/

[9] Michael Saltsman, “Who Really Employs Minimum-Wage Workers?” The Wall Street Journal, October 28, 2013, https://www.wsj.com/articles/who-really-employs-minimumwage-workers-1383001775?mod=wsj_streaming_stream&tesla=y

[10] “2012 SUSB Annual Data Tables by Establishment Industry,” United States Census Bureau, https://www.census.gov/data/tables/2012/econ/susb/2012-susb-annual.html

[11] “Shares of Gross Output by Industry,” Industry Data, Interactive Data, Bureau of Economic Analysis, https://www.bea.gov/itable/

[12] We estimated that the average profit of businesses with fewer than 20 workers in Illinois is roughly $200,000 using data from the Census Bureau and the Bureau of Economic Analysis (BEA). The Census Bureau’s 2012 Statistics of US Businesses provides estimates of number of firms, total annual payroll costs, and total estimated receipts by firm employment size in each state. Using these data we estimated average annual payroll costs and average estimated receipts per business with fewer than 20 employees in Illinois. We then estimated average profit by assuming that the average firm’s profit margin matched gross operating surplus as a percent of gross output in the US private sector, which is reported by the BEA’s industry KLEMS data.

[13] Jared Walczak & Joseph Henchman, “Illinois Considers an 11.25 Percent Tax on Small Businesses,” Tax Foundation, April 26, 2016, https://taxfoundation.org/illinois-considers-1125-percent-tax-small-businesses/

[14] Elizabeth Campbell, “Illinois Morass Fuels Speculation It’ll Be First Junk-Bond State,” Bloomberg Markets, April 21, 2017, https://www.bloomberg.com/news/articles/2017-04-21/illinois-morass-fuels-speculation-it-ll-be-first-junk-bond-state

[15] Alexia Elejalde-Ruiz, “New Illinois $15 minimum wage bill reopens wage fight,” Chicago Tribune, March 13, 2017, http://www.chicagotribune.com/business/ct-illinois-15-minimum-wage-0312-biz-20170311-story.html

[16] Joseph J. Sabia & Than Tam Nguyen, “The Effects of Minimum Increases on Means-Tested Government Assistance,” Employment Policies Institute, December 2015, https://www.epionline.org/wp-content/uploads/2016/01/EPI_MW_GovtAssist_Study_V2-5.pdf

[17] Douglas Holtz-Eakin & Ben Gitis, “Counterproductive: The Employment and Income Effects of Raising America’s Minimum Wage to $12 and to $15 Per Hour,” American Action Forum, July 27, 2015, https://www.americanactionforum.org/research/counterproductive-the-employment-and-income-effects-of-raising-americas-min/

[18] David Neumark, J.M. Ian Salas, & William Wascher, “Revisiting the Minimum Wage-Employment Debate: Throwing Out the Baby with the Bathwater?” NBER Working Paper, January 2013, http://www.nber.org/papers/w18681

[19] John J. Horton, “Evidence form a Minimum Wage Experiment,” New York University, January 2017, http://john-joseph-horton.com/papers/minimum_wage.pdf

[20] Thomas MaCurdy, “How Effective Is the Minimum at Supporting the Poor?” Journal of Political Economy, Vol. 123, No. 2, April 2015, pp. 497-545, http://www.jstor.org/stable/10.1086/679626?&seq=1#page_scan_tab_contents

[21] Dara Lee Luca & Michael Luca, “Survival of the Fittest: The Impact of the Minimum Wage on Firm Exit,” Harvard Business School NOM Unit Working Paper No. 17-088, April 2017, https://papers.ssrn.com/sol3/papers.cfm?abstract_id=2951110