The Daily Dish

October 7, 2024

A Modest Proposal for 2025 Tax Reform

As loyal readers of Eakinomics are aware, the vast majority of the provisions of the 2017 Tax Cuts and Jobs Act (TCJA) will expire at the end of 2025. This provides an opportunity to keep attractive provisions, certainly, but more broadly to undertake another round of tax reform.

Of particular interest in such an effort would be the taxation of income from pass-thru entities (S-corporations, limited liability companies, partnerships, and so forth). Since more than half of business income is taxed as pass-thru income, it is a central part of the U.S. approach to taxing business income.

Now the good news is that the TCJA’s corporation income tax provisions are permanent. Thus, while they might be tweaked, they are largely successful and need little attention. The focus instead should be on providing comparable tax treatment to pass-thru income so there is the same effective marginal tax rate on the return to capital invested in the corporate and the pass-thru sectors.

What would that look like? It takes a little math, so have a second carafe of coffee and bear with me.

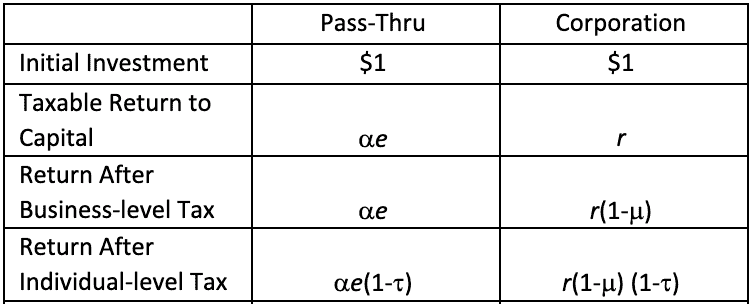

A dollar invested in the corporate sector earns a return, r, which is then taxed at the corporation income tax rate, t (currently 21 percent). The after-tax dollars are then distributed to shareholders as either dividends or capital gains and taxed at the preferential rate, m (currently 20 percent). This is shown on the right side of the table (below).

Consider, now, a pass-thru entity. Suppose it earns e on each dollar invested. For purposes of calculating taxes, assign a share of the earnings, a, as the return to capital investment, which are then taxed at the preferential tax rate just like distributions from corporations. Comparing the computations in the left and right columns, the after-tax returns to the $1 investment are identical when:

ae(1-†) = r(1-µ) (1-†).

Solving implies that the administratively set share (a) be set according to:

a = (r/e)(1-µ).

Notice, however, that total return (e) for the pass-thru is the sum of return to capital (r) and return to labor (l), so this is just:

a = (r/(r+l))(1-µ).

In other words, the key parameter, a, is simply the after-corporate-tax share of capital in income.

If we use the conventional assumption that the share of capital is 0.3 and the corporate tax rate is 0.21, then the key value is a = 0.237. This approach dramatically simplifies pass-thru taxation. Simply take 23.7 percent of the overall earnings and tax it at the dividends and capital gains rate of 20 percent.

The main advantage to this approach is economic efficiency, with the tax code no longer distorting the choice between corporate and non-corporate investments. The return to pass-thru capital investments is taxed at a single rate, scaled to be comparable to the overall tax on corporate investments. In contrast, the current system provides a 20-percent deduction, which translates into a different tax rate for each tax bracket, with none guaranteed to match the after-tax return from the corporate sector.

The idea sketched above is far from a complete proposal, but it demonstrates that there are alternative approaches that could be on the table in 2025. Given the economic circumstances – sub-par trend growth and high federal debt – a premium should be placed on efficient, pro-growth tax systems.

Fact of the Day

The September U-6 (the broadest measure of unemployment) ticked down 0.2 percentage points to 7.7 percent in August.