The Daily Dish

August 26, 2024

S-Corporations

Eakinomics loves this! We’re gonna talk taxes! So sit down, pour yourself a beautiful carafe of coffee, and settle in for the fun. In all seriousness, the topic is going to be “A Primer: The TCJA and S Corporations” by AAF’s Jordan Haring. Why? Because of three key facts regarding S corporations:

- An S corporation does not pay the corporate tax. Instead, it passes its profits on to its shareholders who pay tax on their share of the profits on their individual income (and payroll) tax returns.

- The Tax Cuts and Jobs Act (TCJA) created a new deduction equal to 20 percent of qualified business income for entities like S corporations that pass their income through to be taxed on owners’ returns. That deduction – and a slew of other TCJA provisions – will expire at the end of 2025 unless Congress acts.

- Per Haring: “The S corporation has become the dominant business structure in the United States; the number of businesses classified as an S corporation increased by 839 percent between 1980 and 2021, growing from about 545,400 to over 5.1 million.”

If you string together (1) through (3), you must reach the conclusion that the most significant tax policy issue facing the dominant form of business in the United States is the structure of the individual income tax – not the corporation income tax – and it is almost entirely up for grabs next year.

Haring does a beautiful job of covering the evolution of S corporations, but for Eakinomics’ purposes, let us just get on the record who can be an S corporation:

To qualify for S corporation status, a business must meet the following criteria: 1) it must be a domestic (U.S.) corporation; 2) it must have only allowable shareholders (this includes individuals who are U.S. citizens or residents, estates, certain trusts (grantor trusts, testamentary trusts, voting trusts, electing small business trusts, or qualified Subchapter S trusts)); 3) it must have 100 or fewer shareholders; 4) it must have only one class of stock; and 5) it must not be an ineligible corporation (certain financial institutions, insurance companies, and domestic international sales corporations are ineligible for S corporation status).

Haring also covers the waterfront of payroll taxes, state taxes, and limitations on the 20 percent deduction. But the heart of the debate will hinge on the business tax implications of the desire of populists to soak the rich. She notes that:

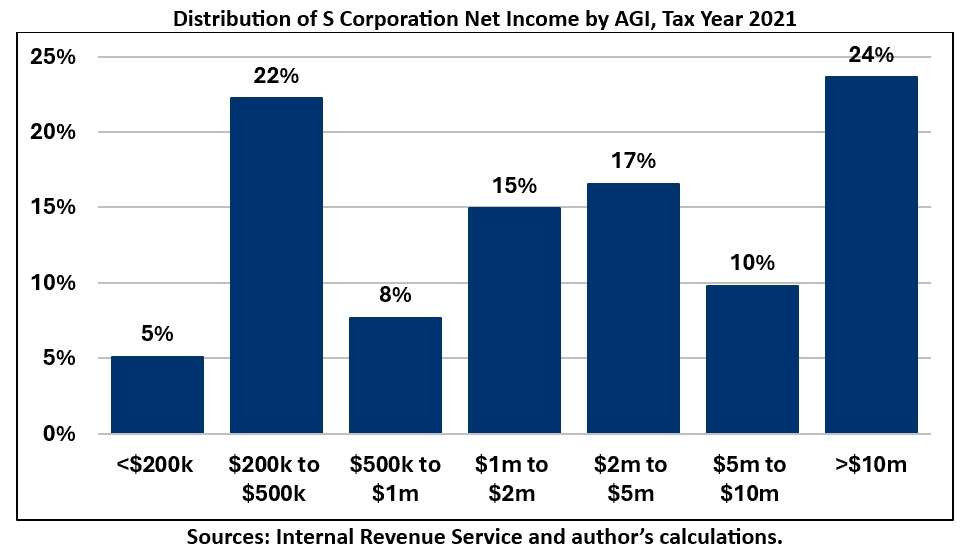

In tax year 2021, the last tax year for which comprehensive data from the IRS is available, 5.3 million federal individual income tax returns reported receiving nearly $674 billion of net income from S corporations. Taxpayers with an adjusted gross income (AGI) of $200,000 or greater earned just over 95 percent of S corporation income, while accounting for roughly 36 percent of returns reporting income from an S corporation. Conversely, taxpayers with an AGI of less than $200,000 earned about 5 percent of S corporation income but accounted for roughly 64 percent of returns reporting S corporation income.

In other words, the top rate is an important business tax rate. But note that essentially every tax rate in the rate structure matters for business decisions (see the chart, reproduced from her paper).

Tax policy experts worry about the structure of taxes because it can alter the incentives to be an S corporation versus some other form, to invest in capital, to undertake R&D, and to hire and train workers. A tax system that is as neutral as possible – that is, has the same effective tax rate on dollars allocated to these activities – will interfere the least with business decisions. This is the goal of pro-growth tax reforms.

The obvious problem is that there are many tax rates associated with S corporation income, as well as the problem of keeping the playing field level with C corporations. That is the tax policy challenge of 2025.

So, read the entire primer and enjoy that second carafe of coffee.

Fact of the Day

A national 5 percent cap on rent growth would not lower overall costs and could result in between $3,500 and $6,000 in additional costs for renters over a five-year period.